What Is a Mega Backdoor Roth?

A mega backdoor Roth allows you to contribute up to $70,000 annually to retirement accounts by making after-tax 401(k) contributions and converting them to Roth accounts for tax-free growth.

If you’re maxing out your standard retirement contributions and want to save even more in tax-advantaged accounts, the mega backdoor Roth strategy could be a powerful tool. This advanced retirement savings approach lets high-income earners bypass normal contribution limits and build substantial Roth account balances. However, it requires specific plan features and careful execution to avoid unnecessary taxes.

Why Is It Called "Mega" Backdoor Roth?

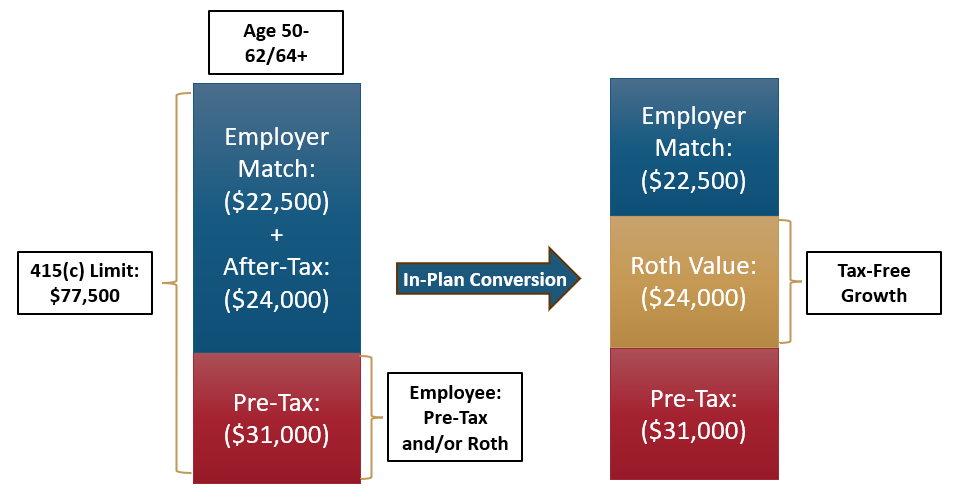

This strategy is called “mega” because it allows for much larger contributions than the traditional backdoor Roth IRA approach. While a regular backdoor Roth is limited to the annual IRA contribution limit of $7,000 in 2025, the mega backdoor Roth can potentially allow contributions up to the total 401(k) limit of $70,000 for those under 50, or $77,500 for those ages 50-59 and 64+, and $81,250 for those ages 60-63.

The strategy works by taking advantage of a lesser-known 401(k) contribution type: after-tax contributions. These are different from both pre-tax and Roth contributions, and they’re subject to the much higher Section 415(c) contribution limit rather than the standard elective deferral limit.

How Does a Mega Backdoor Roth Work?

The mega backdoor Roth involves two main steps: making after-tax contributions to your 401(k) beyond your regular pre-tax or Roth contributions, then converting those after-tax amounts to a Roth account where they can grow tax-free.

Here’s the process:

1. Max out standard contributions

Contribute the full $23,500 to your 401(k) (pre-tax or Roth) in 2025 if you’re under 50

2. Make after-tax contributions

Add additional after-tax contributions up to the total limit of $70,000, minus any employer contributions

3. Convert to Roth

Move the after-tax money to either a Roth 401(k) (in-plan conversion) or a Roth IRA (rollover)

Key advantages of converting to Roth:

Example Scenario

- Salary: $250,000

- Maxes out pre-tax: $22,500

- Receives 9% company match: ~$31,000

- Remaining room: $24,000 for after-tax contributions

- Converts immediately to Roth = $24,000 tax-free growth potential

What Are the 2026 Contribution Limits?

For 2026, the employee elective deferral limit for 401(k) plans is $24,500 for those under 50, with the total contribution limit (including employer contributions) set at $72,000.

Understanding these limits is essential for calculating how much you can contribute through a mega backdoor Roth strategy:

| Contribution Type | 2026 Limit (Under 50) | 2026 Limit (Age 50-59, 64+) | 2026 Limit (Age 60-63) |

|---|---|---|---|

| Employee Deferrals (Pre-tax + Roth) | $24,500 | $32,500 | $35,750 |

| Total Contributions (All Sources) | $72,000 | $80,000 | $83,250 |

| Potential After-Tax Space | $47,500 | $47,500 | $47,500 |

The “after-tax space” shown above represents the maximum you could contribute after-tax, assuming no employer contributions. However, most employees receive some form of employer match or profit-sharing, which reduces the available space for after-tax contributions since all contributions count toward the $72,000 total limit.

It’s important to note that catch-up contributions for those 50 and older are not included in the Section 415(c) limit calculation. The enhanced catch-up for those ages 60-63 allows an additional $11,250 in contributions (instead of the standard $8,000), providing even more opportunity for high earners in this age bracket.

Who Qualifies for a Mega Backdoor Roth?

Your eligibility for a mega backdoor Roth depends entirely on your employer’s 401(k) plan features, not your income level.

Your plan must include all three of these features:

- After-tax contribution option: Your plan must allow you to make non-Roth after-tax contributions beyond the standard $23,500 elective deferral limit

- Roth conversion capability: Your plan must offer either in-plan Roth conversions or allow in-service withdrawals to a Roth IRA

- Available contribution room: You must have space between your current contributions (including employer match) and the $70,000 total limit

Check your plan documents or contact your plan administrator to verify these features. Many 401(k) plans don’t offer after-tax contributions or in-plan conversions because of the administrative complexity and potential compliance testing issues.

Additionally, if you work for a private company (not a government entity), your plan may be subject to IRS nondiscrimination testing called the Actual Contribution Percentage (ACP) test. This test can limit after-tax contributions for highly compensated employees if lower-paid employees aren’t also making substantial after-tax contributions. This is the primary reason why mega backdoor Roth strategies aren’t available in most workplace plans.

Is a Mega Backdoor Roth Worth It?

A mega backdoor Roth is worth considering if you’re a high earner who has already maxed out standard retirement contributions, expects to remain in a high tax bracket, and has access to a plan that supports the strategy.

Before implementing this approach, evaluate these factors:

Financial Readiness:

- Have you maxed out your standard 401(k) contributions ($23,500)?

- Have you fully funded your HSA if you have access to one ($4,300 individual, $8,550 family in 2025)?

- Do you have an adequate emergency fund (3-6 months of expenses)?

- Are you comfortable locking away this money until retirement?

Plan Features:

- Does your 401(k) allow after-tax contributions?

- Does it permit in-plan Roth conversions or in-service withdrawals?

- If applicable, will your after-tax contributions pass the ACP test?

- Does your plan offer automatic conversion features?

Tax Considerations:

- Are you in a high tax bracket now and expect to remain there in retirement?

- Can you afford to pay taxes on any earnings that accumulate before conversion?

- Have you consulted with a tax professional about your specific situation?

Administrative Effort:

- Are you willing to monitor conversions regularly (ideally quarterly or monthly)?

- Can you track the tax implications of your conversions?

- Do you have time to coordinate with your plan administrator?

If you answered “yes” to most of these questions, the mega backdoor Roth could accelerate your retirement savings significantly. If you have concerns about multiple items, traditional investment approaches may be more appropriate for your situation.

Disclosures: All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. This information is provided for educational purposes only and does not constitute tax advice.