Beginning with tax years after December 31, 2025, new federal “Trump accounts” under Internal Revenue Code §530A will give families a dedicated way to build long‑term wealth for children using low‑cost index funds. Think of these as “child IRAs with special funding rules and guardrails” rather than another college savings account.

Unlike traditional custodial accounts that parents can tap for a wide range of expenses, Trump 530A accounts are designed to be locked‑box growth vehicles until a child reaches adulthood, and then to function like a traditional IRA. That structure creates powerful compounding potential but also introduces some planning nuances parents will want to understand.

What Is a Trump (530A) Account?

A Trump account is an IRA established for a child under age 18 that follows special §530A rules until the child turns 18. On paper, it looks like a traditional IRA, but its rules are tailored to children and focused on disciplined, index‑based investing.

The account is legally owned by the child, with a parent, legal guardian, or other authorized individual serving as custodian until age 18. That means the assets belong to the child from day one, but decision‑making authority rests with the adult custodian until the child reaches majority.

Investment Guardrails: Low Cost Index Funds Only

Before age 18, 530A accounts can only be invested in non‑leveraged, low‑cost index mutual funds or ETFs that track broad U.S. equity indexes (for example, an S&P 500 index fund).

These guardrails mean families focus is on broad‑market participation and compounding.

Who Qualifies and How to Open an Account

There are two primary ways to open a Trump 530A account:

- By filing IRS Form 4547 along with the family’s federal income tax return.

- Online through the IRS/Treasury portal, where an authorized individual signs into an IRS online account (via ID.me) and completes Form 4547 electronically or uses the TrumpAccounts.gov portal/app.

This flexibility allows families to align account setup with either their annual tax filing process or a dedicated online workflow during the year.

Contribution Rules and Funding Sources

Trump 530A accounts have a straightforward annual contribution cap but more diverse funding sources than traditional IRAs. Contributions are capped at $5,000 per year before age 18, with the limit indexed for inflation after 2027 and rounded to the nearest 100; there is no above‑the‑line IRA deduction for contributions.

Who can contribute is intentionally broad: parents, guardians, extended family, friends, employers, and qualifying philanthropic or governmental entities may all add to the account. This structure opens the door for family gifting strategies, employer benefit programs, and community or charitable initiatives to all funnel resources into a child’s long‑term wealth fund.

Employer and “General Funding” Contributions

Employers can play a role in funding Trump accounts through structured benefit programs. Up to 2,500 per employee per year (inflation‑indexed) may be excluded from the employee’s income under IRC §128 if the contribution is part of a compliant “Trump account contribution program.”

In addition, government agencies and charitable organizations can make “general funding contributions” that are allocated across defined groups of beneficiaries, such as children born in certain years or living in particular states. This opens the door to large‑scale public‑private initiatives aimed at boosting long‑term savings for entire cohorts of children.

Federal Seed Money: The Pilot Program

Under the “One Big Beautiful Bill” (Public Law 119‑21), eligible children born between January 1, 2025, and December 31, 2028, may receive a federal “seed” contribution of 1,000 into a Trump account. Families do not need to make any personal contribution to receive this pilot funding.

Beyond this initial seed, philanthropists, corporations, and qualifying organizations can layer on additional general funding contributions, often targeting specific regions or birth years. For some children, that means a Trump account could start life with multiple funding sources before family dollars are even added.

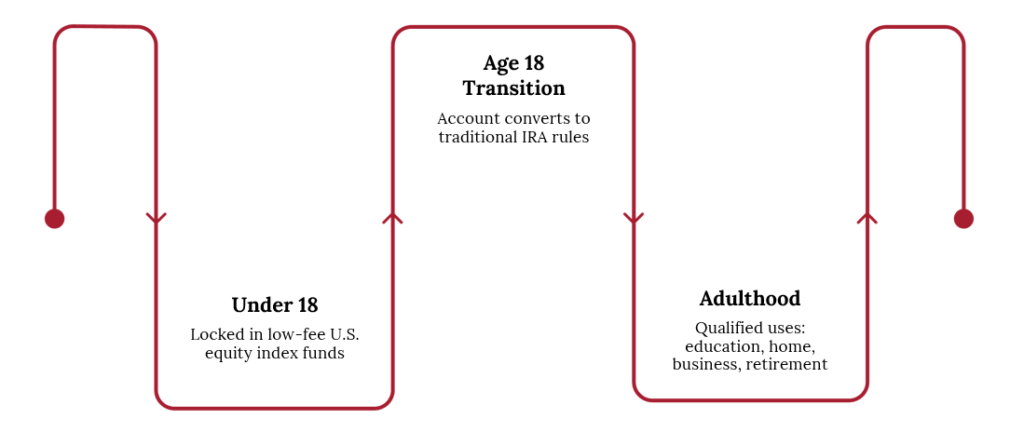

How the Account Evolves Over Time

Trump 530A accounts are deliberately illiquid for minors. Prior to January 1 of the year the child turns 18, assets must remain in qualifying low‑fee U.S. equity index funds and no distributions are permitted, except for narrow cases such as excess contribution corrections or certain rollovers.

On January 1 of the year the beneficiary turns 18, the account transitions to a standard traditional IRA for tax and distribution purposes. From that point forward, the grown child can eventually use the account for common IRA‑style purposes such as education expenses, a first home, starting a business, or retirement—subject to traditional IRA rules and tax treatment.

Special Distribution and Rollover Rules

Trump accounts come with some unique distribution and rollover provisions that are important in planning. Trustee‑to‑trustee rollovers between Trump accounts are permitted, but only as full‑balance transfers; partial rollovers are not allowed.

Excess contributions can be removed without the usual income inclusion, but any net income attributable to the excess is hit with a 100% tax, underscoring the importance of monitoring contribution limits. If the beneficiary dies before age 18, the account ceases to be a Trump account and the fair market value (less investment in the contract) becomes taxable income to the inheritor or the child’s estate.

ABLE Account Rollover: A Special Needs Planning Tool

One standout feature is the ability, at age 17, to transfer the entire Trump account balance directly to an ABLE account for the same beneficiary on a tax‑free basis. This provides a powerful integration point for families engaged in special‑needs and disability planning.

For some clients, the Trump account can serve as a disciplined accumulation vehicle during childhood, with the option to consolidate funds into an ABLE framework just before adulthood.

Estate and Gift Tax Safe Harbor

When you put money into a child’s Trump Account, the IRS treats it like a normal gift for tax purposes. For most families, that means you can fund these accounts as part of your regular giving to kids or grandkids without triggering extra estate or gift taxes.

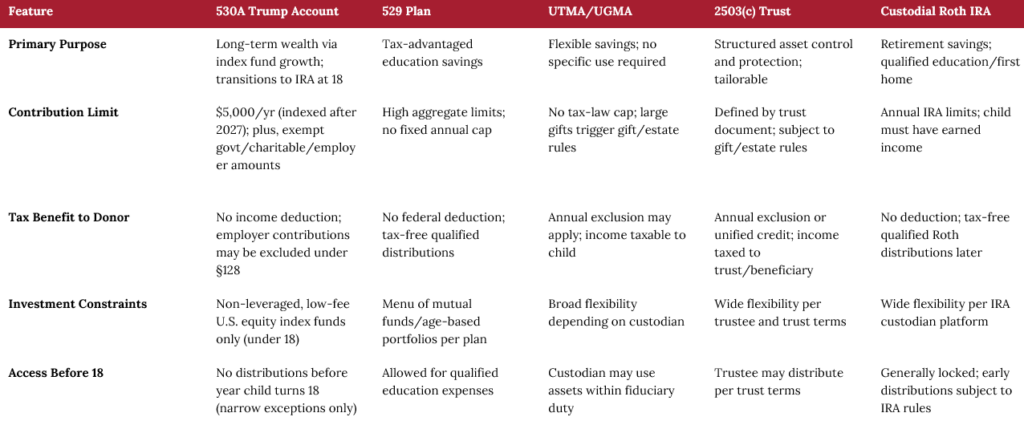

How Trump 530A Accounts Compare to Other Kids’ Accounts

Trump accounts are not a replacement for 529s, UTMAs, trusts, or custodial Roth IRAs—but they do fill a distinct role. Where 529 plans focus on education and UTMAs emphasize flexible access, Trump 530A accounts emphasize locked‑in, index‑fund‑based growth that transitions into a retirement‑style asset at 18.

Key points of comparison include primary purpose, contribution limits, tax benefits, investment flexibility, and access before age 18. For example, 529 plans have high aggregate limits and allow distributions for education expenses, while Trump accounts have a 5,000 annual cap and generally prohibit pre‑18 distributions, but may receive employer, government, and charitable funding that other accounts cannot.

Planning Opportunities for Families

Trump accounts create a distinct planning lane for families who want to build a foundational opportunity or retirement fund for children and grandchildren. By combining government seed money (when available), employer contributions, and family gifts, it is possible to establish a disciplined, long‑term wealth engine that a child cannot access prematurely.

Key Limitations and Considerations

As with any planning tool, Trump Accounts come with trade‑offs. The investment menu is intentionally narrow: at launch, money is invested only in a small set of low‑cost U.S. stock index funds, which won’t suit very risk‑averse families or some special‑needs situations that call for more conservative or flexible investments.

Trump Accounts are also “locked up” while your child is a minor. With very narrow exceptions, you can’t take money out before January 1 of the year your child turns 18, which means less flexibility than UTMA accounts or many trust structures. After that point, the account is treated like a traditional IRA: withdrawals are usually taxed as ordinary income and can trigger a 10% early‑withdrawal penalty before age 59½ unless they fit one of the standard IRA exceptions (such as certain education or first‑home expenses). Rules are new and may be refined over time, so families and advisors should keep an eye on future IRS guidance.

Bringing It All Together

For families motivated to set up long‑term, rules‑based investment accounts for their children—and for employers, charities, and governments looking to support those efforts—Trump 530A accounts add a powerful new option alongside existing tools. Used thoughtfully and coordinated with 529 plans, trusts, ABLE accounts, and broader estate strategies, they can become a cornerstone of intergenerational planning for many households.

Important Disclaimers: Saxon Interests, Inc. is a registered investment advisor. Information in this message is for the intended recipient[s] only.

The information provided is for educational and informational purposes only and does not constitute personalized tax or investment advice and it should not be relied on as such. Tax rules are complex and individual circumstances vary. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. Please consult with a qualified financial advisor and tax professional before making decisions.

Some information throughout this document has been obtained from sources believed to be reliable, but its accuracy is not guaranteed.

Contact us

Get Started Today

Take control of your financial future with confidence. Contact Saxon Financial Group to schedule your consultation and learn how we can tailor a financial plan around your unique needs. Together, we’ll guide you down the most strategic path to achieving financial security and peace of mind.

Tell us how we can help you today