Interest rates play a crucial role in determining the value of pension funds and retirement savings, influencing everything from lump sum payments to retirement timing decisions. Whether you’re nearing retirement or planning your long-term financial strategies, understanding how shifting interest rates affect these critical financial components is key to making informed choices.

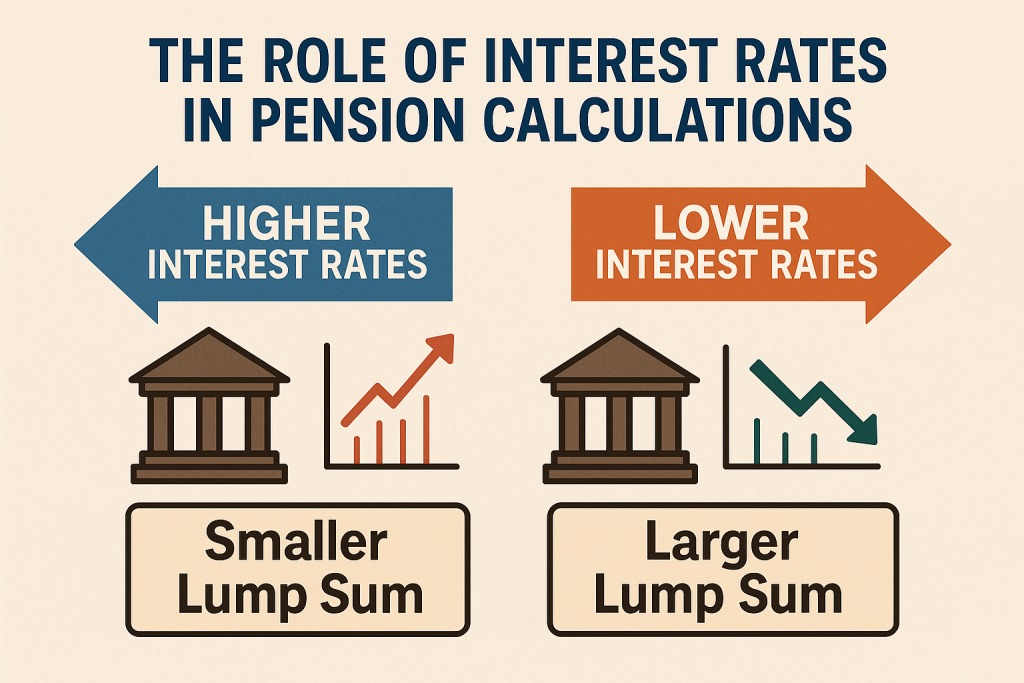

The Role of Interest Rates in Pension Calculations

Interest rates influence lump sum payouts by determining the present value of future pension payments. Here’s how it works:

Pension plans often calculate a lump sum option as the present value of future monthly payments.

For example, a monthly retirement income of $2,000 over 20 years is translated into a single upfront payment. To arrive at that lump sum, pension funds “discount” these future payments to their present value using the current interest rate.

Higher interest rates result in smaller lump sums.

When rates rise, future payments are discounted more heavily (they’re considered “worth less” today), leading to a smaller lump sum payout.

Lower interest rates result in larger lump sums.

Falling rates increase the present value of future payments, giving retirees a more attractive lump sum option.

Interest Rates and Pension Types

The degree to which interest rates affect pensions depends on the type of retirement plan. Here are the two most common plan types:

1. Defined Benefit Plans: These traditional pension plans promise a fixed monthly payment upon retirement. While monthly payments remain unaffected by interest rates, the lump sum equivalent of these payments fluctuates significantly depending on current rates.

For instance, if interest rates rise, opting for annuity payments (monthly installments) may become a better choice than taking a lump sum. However, during periods of low rates, the lump sum option becomes more appealing.

2. Cash Balance Plans: These are hybrid retirement plans where participants have an account balance that earns interest credits. Instead of being tied to monthly payment promises, the lump sum is determined differently, making these plans less sensitive to large fluctuations from interest rate changes.

Lump Sum vs. Annuity Decisions

For retirees offered the choice between a lump sum and a monthly annuity, interest rates can significantly influence their decision.

When rates rise, lump sum amounts decrease, making the consistent income from annuity payments more attractive.

When rates fall, lump sum amounts increase, encouraging retirees to take the upfront payout for potential investment growth or immediate liquidity.

Impacts on Retirement Timing

Changes in interest rates can also influence retirement timing decisions, as individuals aim to optimize their payout:

Rising Interest Rates: If rates are climbing, delaying retirement might avoid accepting a reduced lump sum payout.

Falling Interest Rates: If rates are declining, retiring sooner may lock in a higher lump sum value.

Being aware of these factors gives retirees greater control over their financial strategy.

Additional Factors to Consider

While interest rates are a significant driver, other factors also play an important role in pension calculations:

IRS Regulations: The Internal Revenue Service (IRS) publishes interest rates used in pension calculations. These rates often fluctuate, affecting lump sums offered by plans.

Plan Design Variations: Some plans base interest rate usage on a rolling average, while others reset the rate calculation on specific dates. Understanding how your plan determines its rates is critical to accurate planning.

Inflation Impact: Interest rate changes indirectly impact purchasing power. With high inflation, even a “generous” lump sum may lose value over time, eroding savings more quickly.

Key Takeaways for Retirees

Track interest rates: Stay informed about current rates and how they impact your pension. Timing decisions can make a significant difference in the value of your retirement payout.

Consult your plan documents: Understand the specifics of your pension calculation, including whether your plan uses a rolling average or resets interest rates annually.

Consider pairing strategies: For some, opting for a combination of a reduced lump sum and annuity payments offers a good balance of liquidity and long-term income.

Seek professional guidance: Working with a financial advisor can help you evaluate your options based on current market conditions, inflation rates, and personal goals.

Final Thoughts

Interest rates are more than just a fluctuating number on the financial news. For anyone with retirement savings or a pension plan, they can significantly affect how much you receive and when you should retire. By understanding the interplay between rates and pension values, you can make smarter, more confident decisions about your future.

The information provided is for educational purposes only and does not constitute personalized financial, tax, or legal advice. Investment advisory services are offered through Saxon Financial Group, an SEC-registered investment advisor. All investing involves risk. Please consult with your financial advisor, tax professional, or attorney before making decisions based on this content.

Contact us

Get Started Today

Take control of your financial future with confidence. Contact Saxon Financial Group to schedule your consultation and learn how we can tailor a financial plan around your unique needs. Together, we’ll guide you down the most strategic path to achieving financial security and peace of mind.

Tell us how we can help you today