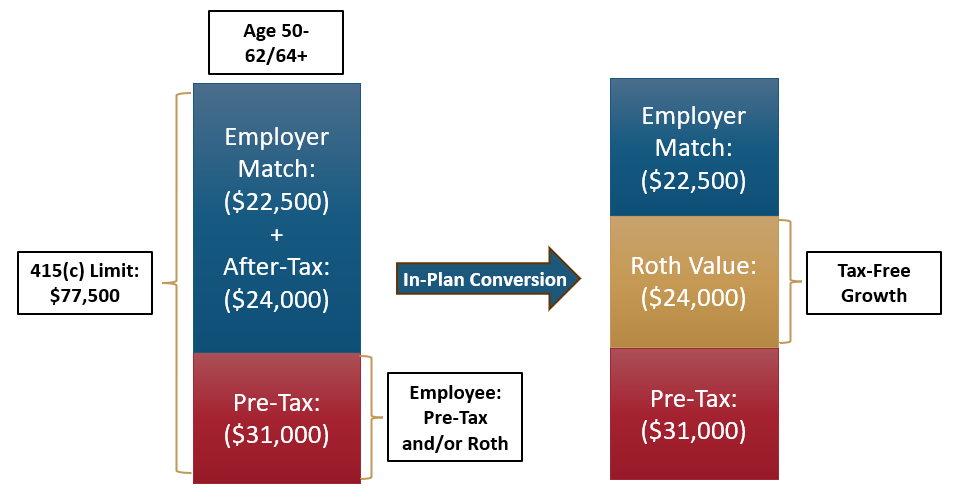

After making your after-tax contributions, you need to convert them to a Roth account. There are two ways to do this based on your 401(k) plan’s options:

In-Plan Roth Rollover

If your 401(k) plan supports it, you can directly convert your after-tax contributions into a Roth 401(k) within the same plan.

Roth IRA Conversion

Alternatively, you can roll over your after-tax contributions into a Roth IRA. This option is particularly attractive because Roth IRAs have fewer withdrawal restrictions than Roth 401(k)s.

Tip: Earnings on after-tax contributions are treated as pre-tax: While your after-tax contributions themselves have already been taxed, any earnings they generate within the employer plan are considered pre-tax money. The best practice is to convert after-tax contributions to a Roth account (either Roth 401(k) or Roth IRA) as soon as possible, ideally before substantial earnings accumulate. This minimizes taxable income triggered by the conversion and maximizes the amount growing tax-free in the Roth account moving forward.

Important: Saxon Financial Group Does Not Service Existing Plans. We are an independent financial advisory firm. We do not manage, administer, or have access to your existing pension, 401(k), or employer retirement plan. For address changes, beneficiary updates, account balances, or plan-related questions, contact your plan administrator or employer’s HR department directly.

Important: Saxon Financial Group Does Not Service Existing Plans. We are an independent financial advisory firm. We do not manage, administer, or have access to your existing pension, 401(k), or employer retirement plan. For address changes, beneficiary updates, account balances, or plan-related questions, contact your plan administrator or employer’s HR department directly.