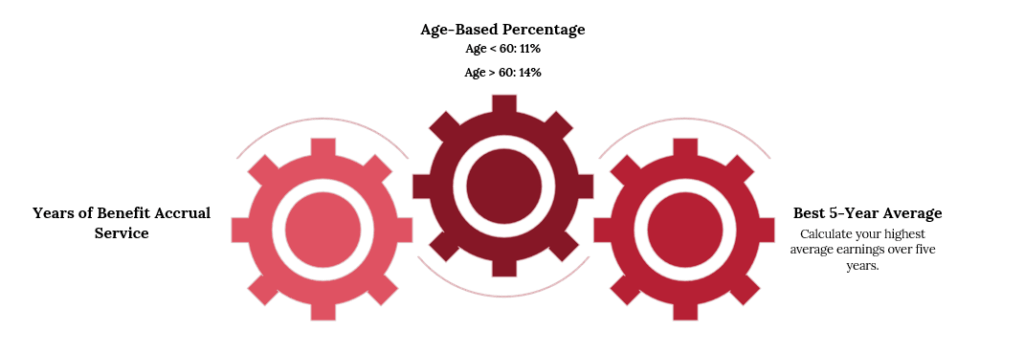

If you were hired, rehired, or first became eligible for the Chevron Retirement Plan before January 1, 2008, you are covered by specific provisions of the plan. Your retirement benefit is determined using a formula that incorporates your Highest Average Earnings, the years of Benefit Accrual Service, and a Social Security offset. This means your benefit grows as your years of service, age, and salary (including base pay and Chevron Incentive Plan (CIP) pay) increase.

Social Security Offset: The plan uses an “offset” method, integrating your pension benefit with Social Security. When starting your benefit, you can choose to provide documentation of your actual Social Security earnings history for a more precise offset calculation or have Chevron estimate the earnings. Review the Social Security Offset section in the plan description for important details to help make your decision.

Traditional Pension with Social Security Integration: your CRP benefits follow the traditional Social Security integrated approach – a time-tested formula that coordinates your pension with expected Social Security benefits.

Formula: based on your Highest Average Earnings and years of service. We multiply your highest average salary by 1.6% and then by your total years of service. From that, we subtract a Social Security offset. For example, if your Highest Average Earnings are $100,000 and you have 30 years of service, the calculation is 1.6% times 100,000 times 30, giving you $48,000 per year before the offset. Key things for this group: early retirement may reduce the benefit if you start before age 60

How Your Benefits Build

Note: Early retirement is available starting at age 55 with 15+ years of service, though benefits are significantly reduced. These reductions are permanent and affect your lifetime income, so careful consideration of the financial impact is essential before making this decision.

Important: Saxon Financial Group Does Not Service Existing Plans. We are an independent financial advisory firm. We do not manage, administer, or have access to your existing pension, 401(k), or employer retirement plan. For address changes, beneficiary updates, account balances, or plan-related questions, contact your plan administrator or employer’s HR department directly.

Important: Saxon Financial Group Does Not Service Existing Plans. We are an independent financial advisory firm. We do not manage, administer, or have access to your existing pension, 401(k), or employer retirement plan. For address changes, beneficiary updates, account balances, or plan-related questions, contact your plan administrator or employer’s HR department directly.