Key Features of Shell’s Retirement Plan

Shell provides employees with one of the most robust retirement savings programs in the industry. These features are designed to help you build wealth and create a strong foundation for retirement.

Important: Saxon Financial Group Does Not Service Existing Plans. We are an independent financial advisory firm. We do not manage, administer, or have access to your existing pension, 401(k), or employer retirement plan. For address changes, beneficiary updates, account balances, or plan-related questions, contact your plan administrator or employer’s HR department directly.

Important: Saxon Financial Group Does Not Service Existing Plans. We are an independent financial advisory firm. We do not manage, administer, or have access to your existing pension, 401(k), or employer retirement plan. For address changes, beneficiary updates, account balances, or plan-related questions, contact your plan administrator or employer’s HR department directly.

Saxon helps you build a strategy around your benefits — we do not service them.

The Shell Provident Fund 401(k)

The Shell Provident Fund 401(k) plan is designed for U.S. employees, providing robust retirement savings tools and flexible contribution options to fit your personal financial goals.

Key Features

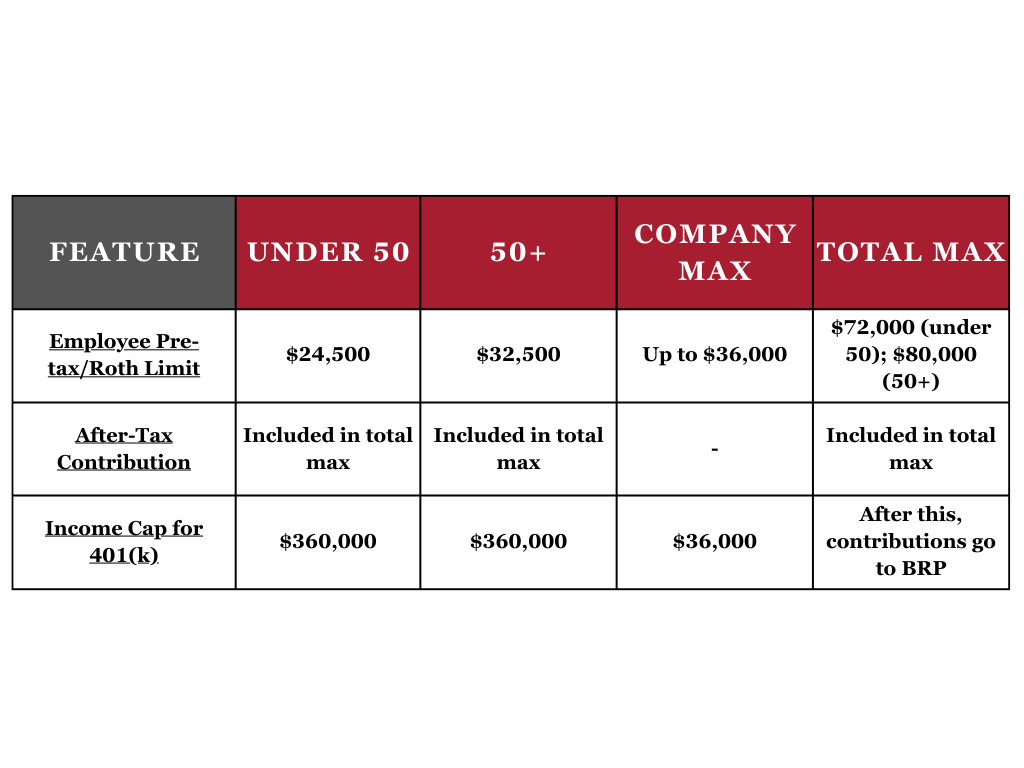

Eligibility & Participation: Immediate eligibility and 100% vesting for all employee and employer contributions. New hires are auto-enrolled at a 3% pre-tax contribution rate but can change this at any time via Fidelity NetBenefits.

Administration: Managed through the Fidelity NetBenefits platform, offering robust online account management and education tools.

Contribution Types

Employee Contributions

- Pre-Tax and Roth 401(k):

- Under age 50: Up to $24,500 total for 2026.

- Age 50 or older: Additional $8,000 catch-up, for a total of $32,500.

- After-Tax (Non-Roth):

- Employees may contribute up to $11,500 after-tax, limited by the annual total contribution cap.

- Total Employee + Employer Contribution Cap:

- $70,000 for those under 50, $77,500 for those over 50, per current IRS rules and Shell policy.

- Contribution Changes:Change your contribution rate or type at any time via NetBenefits.

Employer Contributions

- Company Matching:

- Shell contributes between 2.5% and 10% of annual cash compensation, depending on your length of service (10% after 9 years).

- Employer Contribution Cap:

- Maximum of $36,000 for 2026, based on the IRS income limit of $360,000 annual compensation.

- Above IRS Limit:

- If earnings exceed $360,000, further contributions shift to the Shell Provident Fund Benefit Restoration Plan (BRP

Strategy Highlight: BrokerageLink

A BrokerageLink strategy inside Shell’s 401(k) uses the plan’s self‑directed brokerage window at Fidelity to build a more customized, diversified portfolio while keeping all the tax benefits of the 401(k). It is typically best suited for experienced investors or those working with an advisor who want access to a broader, often lower‑cost fund universe than the standard Shell core options.

The Shell Provident Fund Benefit Restoration Plan

For employees who exceed the income contribution limits of the qualified 401(k) plan, Shell credits additional contributions to the BRP after reaching $360,000 in income for 2026

Key Benefits of the BRP

Restoration of Retirement Benefits Shell uses the BRP to “restore” the contributions lost due to IRS-imposed limits. Any contributions above the threshold for the 401k or Pension plan are deposited into a separate, non-qualified account under the BRP. This ensures your total retirement savings align with your income and benefit plan goals.

Tailored Solutions for Different Pensions

The BRP is not a one-size-fits-all plan. There are separate BRPs designed to mirror different pension plans, such as the 80 Point Pension and the APF Pension. This alignment ensures continuity in your retirement contributions across all plans.

Maximized Retirement Savings

By supplementing your qualified plan contributions, the BRP helps you save more for retirement, ensuring you don’t miss out on reaching your long-term financial goals.

Understanding the BRP

IRS Limits on Retirement Contributions: The IRS places annual limits on how much money can be contributed to qualified retirement plans like 401k and Pension plans. These limits are typically tied to income levels and can cap contributions for high-income earners well before they reach their potential savings goals.

Non-Qualified Plans: For employees affected by these limits, non-qualified plans like the BRP provide a way to make up for the shortfall in retirement benefits. Think of it as an extension of your retirement plan that picks up where the IRS rules leave off.

Tax Implications: It’s important to note that the BRP is a non-qualified plan, meaning it functions differently from qualified plans when it comes to taxes. Distributions from the BRP are taxable at the time they are paid out, so it’s crucial to factor this into your overall retirement planning.

Timing Matters :The timing of your retirement can significantly impact the after-tax value of your BRP payouts. Coordinating your retirement date with the structure of your BRP distributions can help maximize the financial benefit you receive.

Summary Table (2026 Key Limits)

Why Timing and Planning Are Critical

If you’re a high-income earner at Shell, understanding how and when to utilize the BRP is vital for getting the most value out of your retirement benefits. Teaming up with financial professionals who specialize in retirement planning can help you optimize your BRP contributions, timing, and tax strategies.

Notable Features

The Shell Provident Fund allows employees to make extra after-tax contributions beyond standard 401(k) limits and then convert these contributions to a Roth account—either within the plan or by rolling to a Roth IRA. This strategy, known as the “Mega Backdoor Roth,” lets you grow both contributions and future earnings entirely tax-free, provided you follow IRS rules (hold the Roth account at least five years and be 59½ or older when withdrawing).

To maximize benefits, first fill your pre-tax/Roth 401(k) cap, then add after-tax contributions, and convert these promptly to minimize any taxable gains. Only after-tax funds (not employer matches or pre-tax dollars) can be converted. This technique is especially valuable for high earners who want to save more in tax-advantaged Roth accounts, offering significant long-term tax savings and flexibility. Proper timing and understanding plan rules are essential—consult a knowledgeable advisor to ensure you get the most value from this advanced Shell 401(k) feature.

When you hold Shell company stock in your Shell Provident Fund 401(k), you may benefit from a valuable tax strategy known as net unrealized appreciation (NUA):

If you take the stock “in kind” as a lump-sum distribution (not by selling or rolling it to an IRA), you pay ordinary income tax only on the original cost basis of your shares at the time of distribution.

The increase in value (NUA) between your cost basis and the stock’s market value at distribution is not taxed immediately. When you eventually sell the stock, the NUA portion is taxed at long-term capital gains rates, which are typically much lower than ordinary income tax rates.

Any further growth in the stock’s value after you move it to your brokerage account is also taxed as capital gains, depending on your holding period after distribution.

This approach can significantly reduce taxes—especially if your Shell shares have grown substantially in value—by converting a large part of your retirement savings from ordinary income tax rates to more favorable capital gains rates. However, NUA isn’t right for everyone and requires careful handling; you must distribute your entire 401(k) balance for NUA to apply, and the process is complex. Always consult a tax advisor to see if this strategy fits your retirement goals and tax situation.

Additional Benefits

Shell’s 80-Point Pension Plan offers employees a reliable monthly retirement income. You’re eligible when your age plus years of Shell service reach 80 points and you’re at least 50. The benefit is calculated as 1.6% of your average highest three years’ pay (within your last ten years) times your years of service. The plan includes options for early and special retirement, coordinates with Social Security benefits, and has a Benefit Restoration Plan to ensure equitable benefits even for high earners affected by IRS limits.

The Shell APF Pension Plan gives you a retirement benefit based on a percentage of your salary earned each year (ranging from 3% to 16%, increasing with your age and years of service), multiplied by your average highest pay over 36 consecutive months in your last 10 years. You’re fully vested after three years, and when you retire or leave Shell, you can choose either a lump sum or a monthly lifetime payment. The plan is portable and flexible, providing clear, rewarding retirement income tied to your career growth.

The Shell GESPP enables eligible employees to purchase Shell shares at a 15% discount, offering a direct way to invest in the company’s future. Employees can contribute through regular payroll deductions or a lump sum, up to an annual cap, with shares bought at the lowest value of the plan year plus the additional discount. Participants benefit from potential stock appreciation and dividend payments, and enjoy flexibility in how they contribute. While the program offers a convenient and potentially rewarding way to build wealth and share in Shell’s success, employees should be aware of investment risks and possible tax implications, and are encouraged to review the plan’s terms and consult a tax advisor as needed.

Take the Next Step

Shell’s retirement benefits offer incredible opportunities to secure your financial future, but making the most of them requires expert planning. With Saxon Financial by your side, you’ll have the support you need to unlock the full potential of your retirement package.

Get in touch with Saxon Financial today to schedule a consultation. Together, we’ll build a retirement plan that provides peace of mind and long-lasting financial security.

Disclosures: Saxon Financial Group is not affiliated with or endorsed by Shell. Corporate benefits may change at any time. Be sure to consult with human resources and review your plan summary before making a decision.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. This information is provided for educational purposes only and does not constitute tax advice.

Contact us

Get Started Today

Take control of your financial future with confidence. Contact Saxon Financial Group to schedule your consultation and learn how we can tailor a financial plan around your unique needs as an Oil & Gas professional. Together, we’ll guide you down the most strategic path to achieving financial security and peace of mind.

Tell us how we can help you today

By providing a telephone number and submitting the form, you consent to be contacted via SMS from Saxon Interests Inc. Message frequency may vary. Message & data rates may apply. Reply STOP to opt out of further messaging. Reply HELP for more information.