The recently signed 900-page tax and spending law—H.R. 1, known informally as the ‘Big, Beautiful’ Tax Bill—marks a turning point in the landscape of American finance and government spending. Signed on July 4, this monumental legislation reaches into nearly every facet of economic life and contains dramatic changes for both individuals and businesses. Below, we take a deep dive into the new law’s most significant provisions, their potential impacts, and what investors, taxpayers, and consumers need to know.

The Big Picture: Fiscal Impact and Timing

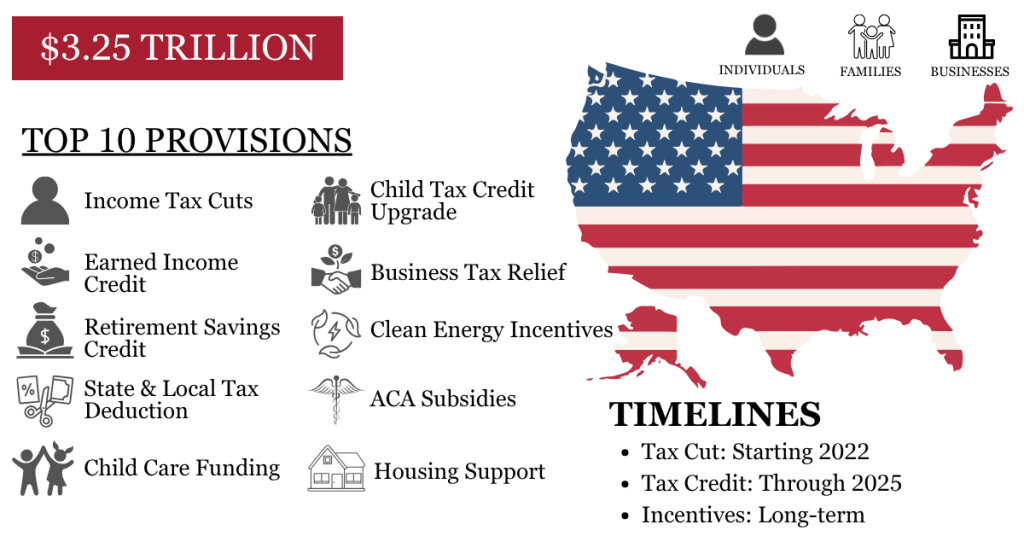

- Price Tag: The law is projected to increase the national debt by $3.25 trillion over the next decade, according to Congressional Budget Office (CBO) estimates, making it the priciest legislative act in U.S. history. This is made up of $4.46 trillion in tax cuts and $1.21 trillion in spending reductions.

- Front-Loaded Costs: The bulk of fiscal stimulus occurs up front, peaking in 2027, due to immediate tax relief. However, spending cuts designed to partially offset these costs are delayed, potentially leading to a significant fiscal challenge (‘fiscal cliff’) around 2029–2030.

- Deficit Risks: If Congress extends temporary tax cuts beyond their current schedules, the deficit impact could exceed official estimates.

Economic Implications

- GDP Growth: The law offers only a minor uptick in the country’s economic growth trajectory. The Joint Committee on Taxation estimates a barely perceptible 3 basis points increase in average GDP growth from 2025–2034 (from 1.83% to 1.86%).

- Short-Term vs. Long-Term: Immediate, front-loaded tax relief gives a modest short-term boost, but this is followed by medium to long-term fiscal tightening, resulting in minimal stimulus and the risk of eventual economic drag.

- Household and Business Finance: Numerous detailed changes to credits, deductions, and eligibility rules mean direct, practical changes for how Americans file taxes and strategize financially.

Key Provisions of the Law

Below, the law’s major components are ranked by fiscal impact, from those with the largest deficit increases to those that yield the greatest savings:

1. Permanent Extension of 2017 Individual Tax Cuts

- Background: The 2017 law reduced both individual and corporate income tax rates. Corporate cuts were permanent, but individual cuts were set to expire at the end of 2025. The new law makes these personal brackets permanent, maintaining rates from 10% to 37% and annual inflation adjustments.

- Examples for 2025:

- Single: 10% rate below $11,925; 37% above $626,350

- Married (joint): 10% below $23,850; 37% above $751,600

- Fiscal Impact: $3.6 trillion over ten years—more than the total net cost of the bill itself, as other provisions net out to some deficit reduction.

2. Permanent Expansion of the Child Tax Credit

- The child tax credit, previously doubled from $1,000 to $2,000 (set to expire in 2025), is made permanent and will rise to $2,200 in 2026, then increase with inflation. The credit phases out for single filers earning more than $200,000 and couples earning more than $400,000.

- Fiscal Impact: $817 billion over ten years

3. Temporary Expansion of SALT Deduction

- SALT (State and Local Tax) Deduction: Cap rises from $10,000 to $40,000 starting in 2025, with a 1% annual increase—but only through 2029. The cap then reverts to $10,000.

- The expanded SALT deduction phases out for incomes above $500,000, but all filers may claim at least $10,000.

- Fiscal Impact: $163 billion, likely higher if Congress prevents reversion.

4. Immediate Deduction of Domestic R&D for Businesses

- New Rule: Businesses can now deduct domestic R&D costs in the year incurred, instead of amortizing over five years, starting in 2025.

- Retroactive Refunds: Small/medium businesses (revenue < $31M) can apply retroactively for 2022–2024.

- Fiscal Impact: $141 billion

5. New Deduction for Seniors (2025–2028 Only)

- Above-the-Line Deduction: Taxpayers 65+ can deduct $6,000 (single) or $12,000 (joint) beginning in 2025, ending in 2028. Most standard deduction filers benefit.

- Phases out for incomes above $175,000 (single), $250,000 (joint).

- Fiscal Impact: $93 billion (could be more if deduction is extended)

6. New Deduction for Charitable Contributions

- Above-the-Line Deduction: Standard deduction takers can claim up to $1,000 (single) or $2,000 (joint) for charitable giving from 2026, on a permanent basis.

- Fiscal Impact: $74 billion

7. No Tax on Tips (2025–2028 Only)

- Deduction: Up to $25,000 in tip income can be deducted by workers in tipping sectors (waitstaff, hospitality, etc.) from 2025–2028. Treasury will set guidelines to prevent abuse; managers probably excluded.

- Phases out for incomes above $150,000 (single), $300,000 (joint).

- Fiscal Impact: $32 billion (could be more if deduction extended)

8. Boosted Semiconductor Plant Tax Credit

- The Advanced Manufacturing Investment Credit (Section 48D) is increased from 25% to 35% for domestic semiconductor facility construction. Project construction must begin by end of 2026.

- Fiscal Impact: $15 billion

Provisions Creating Budgetary Savings

9. Faster Phase-Out of Clean Energy Tax Credits

- Tax credits for clean energy (including those for EVs and solar under the Inflation Reduction Act) will phase out more rapidly.

- EV credit ($7,500 new, $4,000 used): Purchases must occur by September 30, 2025

- Residential solar: Must purchase by December 31, 2025

- Commercial/utility solar: Construction must start by July 2026, finish within four years

- Fiscal Savings: $444 billion over ten years

10. New Work Requirements for SNAP and Medicaid

- SNAP: Work rule extended upward from age 54 to 64, stricter rules for certain groups. States with high error rates may be required to cover some SNAP food costs from 2028.

- Medicaid: New work requirements in ~40 states starting in 2027/2028. Eligible adults must work, volunteer, or train at least 20 hours weekly. Reduced provider taxes for states begin in 2028.

- Combined Projected Savings: $1.03 trillion over ten years—$185 billion from SNAP, $841 billion from Medicaid (dependent on assumed enrollment declines).

Final Thoughts

- The Big, Beautiful Tax Bill introduces sweeping and, in some cases, permanent changes to the tax code, with profound effects on both individual and corporate finances.

- Its front-loaded costs and delayed savings offer immediate stimulus at the risk of future deficit issues, especially if Congress extends temporary provisions beyond scheduled expiration.

- Many measures—such as the expanded SALT deduction, tax-free tips, and senior deductions—are time-limited, and investors should watch for further legislative action.

- As with all financial matters, consultation with professional advisors is recommended to navigate the evolving regulatory landscape.

- Economic and market conditions remain subject to change; investment always carries risks, and no single law can guarantee financial success.

Disclosures: This information is provided for informational purposes only and should not be construed as investment or tax advice. Consult your financial advisor or tax professional for advice tailored to your situation. The content herein is based on sources deemed reliable, but accuracy and completeness are not guaranteed. Laws, forecasts, and opinions are subject to change without notice.

Contact us

Get Started Today

Take control of your financial future with confidence. Contact Saxon Financial Group to schedule your consultation and learn how we can tailor a financial plan around your unique needs. Together, we’ll guide you down the most strategic path to achieving financial security and peace of mind.

Tell us how we can help you today