Exploring ConocoPhillips NUA Options

The ConocoPhillips NUA and Savings Plan (401k) Opportunities

If you’ve built a significant balance of ConocoPhillips stock in your CPSP, ConocoPhillips NUA may help you manage your retirement income more effectively. Understanding ConocoPhillips NUA options is essential for maximizing your after-tax retirement wealth.

ConocoPhillips NUA Strategy Requirements

Here’s what you need to know about utilizing this strategy through your CPSP:

- Lump-Sum Distribution Requirement: To take advantage of NUA, you’ll need to take a lump-sum distribution of your entire vested balance from all qualified plans (e.g., all your 401(k) accounts with ConocoPhillips) within one tax year.

- Qualifying Events: Your distribution must align with a qualifying event. These events include separation from service, turning 59 ½, death, or disability.

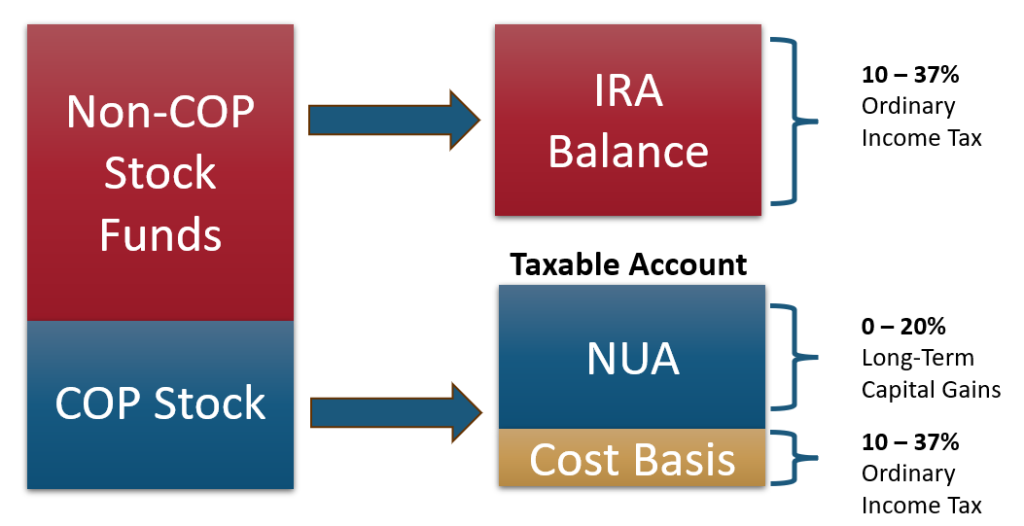

- Transfer as Stock, Not Cash: To utilize NUA, you must transfer the company stock “in-kind” from your 401(k). This means taking the stock as shares, not as cash converted back into shares later.

example scenario

Mark and Lisa Thompson are preparing for retirement after decades of careful saving and planning. Mark spent his career at ConocoPhillips, while Lisa worked in education. They’re now evaluating ConocoPhillips NUA strategies to optimize Mark’s retirement distributions and minimize taxes.

Their ConocoPhillips Retirement Snapshot

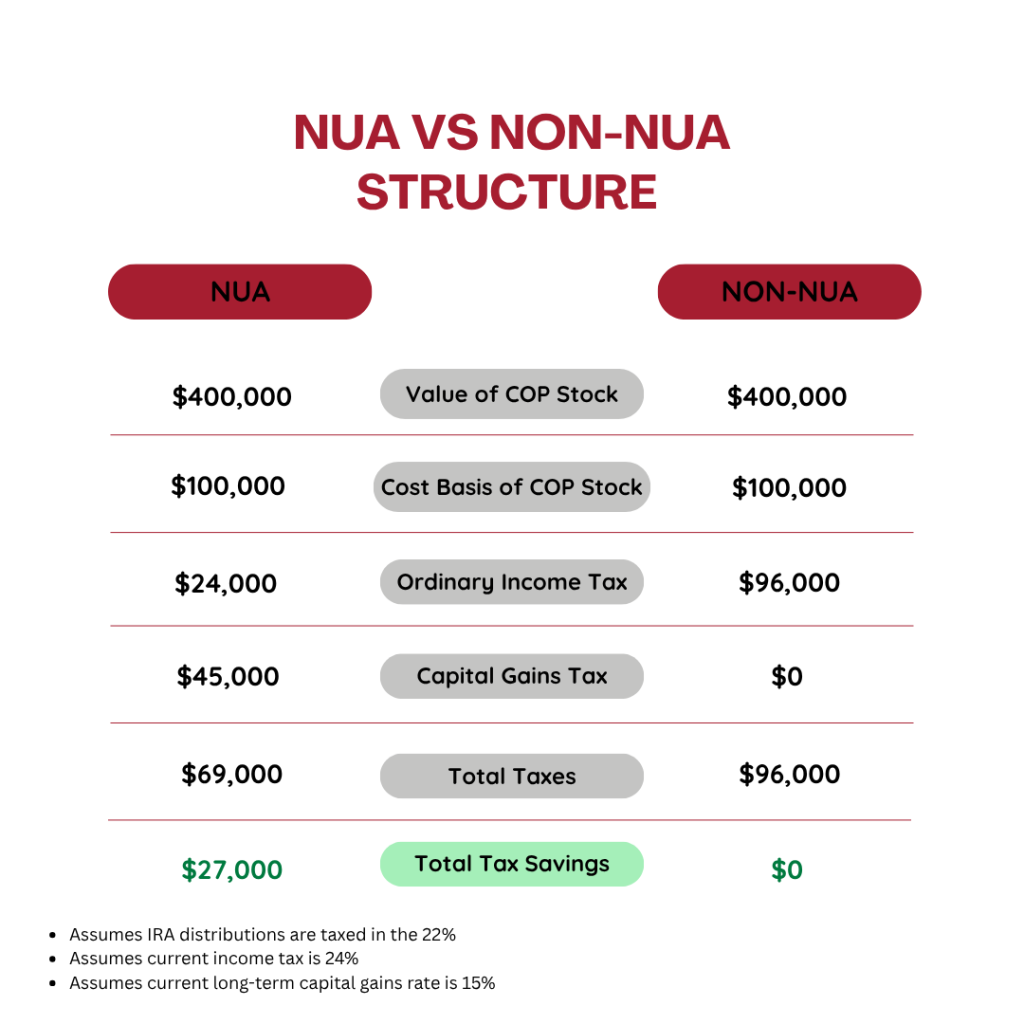

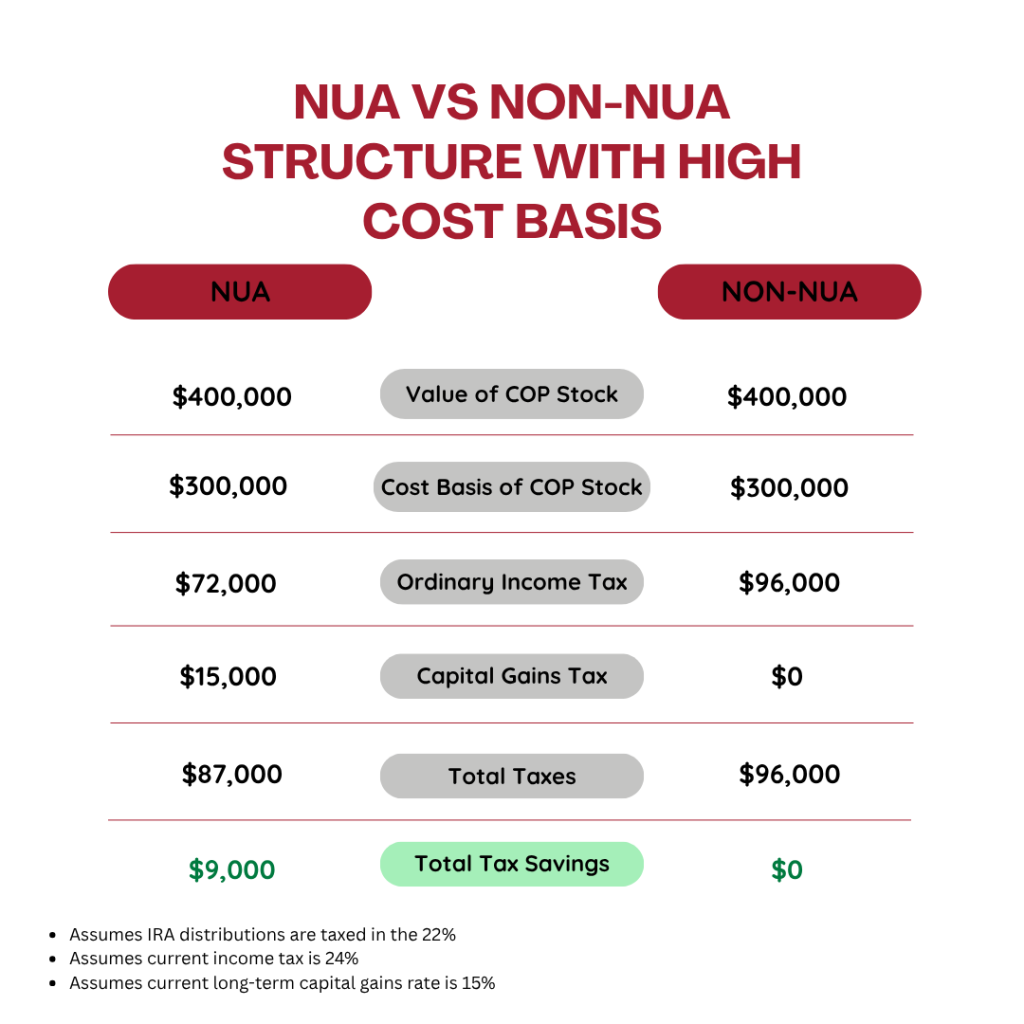

- Total 401(k) Plan Value: $1,000,000

- ConocoPhillips Stock Value: $400,000

- Cost Basis of Stock: $100,000

- Other Retirement Assets: $600,000 (in mutual funds, target date funds, etc.)

Mark is weighing two strategies for the company stock portion of their retirement plan to maximize their after-tax savings.

Their Tax Situation

- While working, their household income places them in the 24% tax bracket.

- After Mark retires, their income will drop, and they expect to be in the 22% tax bracket for IRA withdrawals.

- Their current long-term capital gains tax rate is 15%.

Why NUA Could Be a Game Changer for ConocoPhillips Employees

NUA is a niche tax strategy, but when applied properly, it can result in significant tax savings. Here’s why it’s particularly beneficial for ConocoPhillips employees:

- Lower Tax Rates: By paying lower long-term capital gains tax on the NUA portion instead of the ordinary income tax you’d face if you rolled it into a traditional IRA, you could save a substantial amount.

- Investment Flexibility: Once distributed, you can choose when to sell the company stock, potentially timing the market for additional gains.

- Liquidity Control: Selling strategically over time could help you manage cash flow and minimize tax liabilities year-over-year.

Tax Considerations

Taxation of the NUA after death.

- The NUA portion of the stock will not benefit from the Step-up in cost basis. It will still retain its long-term capital gain status once completed.

- Subsequent gains of the stock will, on top of the NUA, benefit from a step-up in cost basis.

The cost basis of the employer stock is subject to ordinary income.

The NUA is not subject to the 3.8% Net Investment Income tax associated with high earners.

NUAs before Age 59 ½ will be subject to a 10% Early Withdraw Penalty.

NUAs are better with low cost basis stocks vs high cost basis.

What About the ConocoPhillips Pension Plan?

The ConocoPhillips Pension Plan (CPPP) is a defined benefit plan rather than a defined contribution plan like the CPSP. This means your benefit is determined by a formula based on factors such as years of service and compensation, rather than the contributions you’ve made during your career.

Unfortunately, NUA doesn’t typically apply to defined benefit pensions, as these plans don’t involve holding individual stock within the same framework as a 401(k). However, if the CPPP offers a lump-sum distribution option that includes company stock, there could be a specific scenario where NUA might become applicable.

For most employees relying on their pension payouts, it’s crucial to focus on understanding the payout structure, tax implications, and whether a lump-sum or annuity option better suits your financial goals.

Maximizing ConocoPhillips NUA with the Help of a Financial Advisor

Every employee’s financial circumstances are different, making it beneficial to consult a financial advisor to determine if the NUA strategy aligns with your goals. Here’s how a professional advisor can support you:

- Assessing Suitability: The NUA strategy isn’t ideal for everyone. A thorough analysis of your tax situation is critical to decide whether it’s the right fit for you.

- Navigating Tax Complexities: Managing the intricacies of capital gains taxes versus ordinary income taxes can be challenging. An advisor can help you understand these details and their implications.

- Strategic Retirement Planning: It’s vital to not only prepare for retirement but also to deeply understand your plan. An advisor can help integrate the NUA strategy into a broader retirement roadmap.

Final Thoughts

For ConocoPhillips employees and retirees, making the most out of your retirement savings requires careful planning and a sound understanding of the nuances within your plans. Whether leveraging NUA tax savings or understanding your pension options, prioritizing informed financial decisions is key.

If you’re considering NUA as part of your retirement strategy with the ConocoPhillips Savings Plan or just curious how to optimize your retirement benefits, speaking to a financial advisor could be your best next step.

Disclaimer: Tax rules and regulations frequently change and can vary based on individual circumstances. Always consult with a qualified financial advisor or tax professional when making decisions about your retirement and tax planning.

Disclosures: Saxon Financial Group is not affiliated with or endorsed by ConocoPhillips. Corporate benefits may change at any time. Be sure to consult with human resources and review your plan summary before making a decision.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. This information is provided for educational purposes only and does not constitute tax advice.

Contact us

Get Started Today

Take control of your financial future with confidence. Contact Saxon Financial Group to schedule your consultation and learn how we can tailor a financial plan around your unique needs as an Oil & Gas professional. Together, we’ll guide you down the most strategic path to achieving financial security and peace of mind.

Tell us how we can help you today

By providing a telephone number and submitting the form, you consent to be contacted via SMS from Saxon Interests Inc. Message frequency may vary. Message & data rates may apply. Reply STOP to opt out of further messaging. Reply HELP for more information.