Summary

- Both U.S. and international equity markets rallied in the last few days of March to end the month (and the quarter) with positive returns.

- As long-term interest rates stabilized, U.S. bonds recovered most of February’s losses, ending the quarter at January-month-end levels.

- Despite a barrage of economic and policy news, the quarter will be remembered most for the failures of Silicon Valley Bank and Signature Bank.

- Recent bank failures are more a symptom of the Fed’s rapid rate hiking cycle than systemic solvency risk, but they are leading to a sharp contraction in lending that could increase the risks of a recession.

Overview

It certainly hasn’t been a quiet start to the year. Markets started 2023 on a strong note. Both stocks and bonds ended January with decidedly positive returns. However, since then, things have taken a turn for the interesting. In February, most of the gains that stocks and bonds had made since the start of the year were wiped out. In fact, February was the fifth-worst monthly decline for bonds since 1993. Onto the third month of the quarter—March madness indeed. On March 10, Silicon Valley Bank (SVB), the 16th-largest bank in the U.S., collapsed, marking the second-largest bank failure in U.S. history. Two days later, Signature Bank, the 29th-largest U.S. bank, closed down, as customers rushed to withdraw deposits. The speed at which these banks collapsed was unprecedented—a point captured well in a comment from Morgan Stanley CEO James Gorman:

“… with the click of an iPhone, $42 billion left one bank in one day. To give you a sense of the order of magnitude, in the financial crisis of ’08, one bank lost $17 billion in a week, so the rate of withdrawal was 20 times what it was then.

These sentiments were echoed by Federal Reserve Chairman Jerome Powell: “The question we were all asking ourselves over that first weekend was, ‘How did this happen?’”

It happened partly because banks were not offering competitive deposit rates relative to short-term U.S. Treasury rates. As a result, depositors started shifting their money out of bank deposits and into Treasuries while the value of many banks’ assets were declining (also due to higher interest rates). Large banks typically have enough reserves to withstand these shifts, but smaller and more specialized banks struggled to cope with such large drops in their deposit levels, especially at a time when their investments were simultaneously sputtering. Even with these industry-wide headwinds, the largest culprit—at least in the case of SVB—was poor risk management.

In response to the collapse of SVB and the subsequent closure of Signature Bank, the Federal Reserve eased access to its discount window, and banks were able to borrow more than $152 billion from the Fed between March 11 and March 15. The last time banks made extensive use of the discount window was during the Global Financial Crisis, when approximately $111 billion was borrowed at its peak. Following the recent instability in the U.S. financial system, the Fed created a new emergency loan facility, called the Bank Term Funding Program (BTFP). BTFP enables banks to take out loans for up to a year, secured by government bonds, with any collateral valued at par value rather than market prices. This program is designed to provide banks with the necessary liquidity to accommodate deposit withdrawals, which have occurred at an epic pace due to the significant yield differential between what banks are offering as deposit rates and what can be earned by investing in U.S. Treasury Bills. Notably, the average interest earned on a savings account is 0.24% while a three-month T-bill is at 4.77%. Throughout March, deposit withdrawals from commercial domestic banks totaled almost $400 billion while a similar $367 billion flowed into Treasury money markets.

March 17 marked the one-year anniversary of the Fed’s first rate hike of the current hiking cycle. Although it is slowly easing, inflation remains well above the Fed’s 2% target. Throughout the past quarter, a strong labor market and robust spending rates continued to thwart the Fed’s efforts to slow the economy enough to get inflation under control. To date, there are few signs that the labor market is easing. The unemployment rate has remained steady at 3.5%. Until recently, it was relatively easy for the Fed to react quickly to stresses in the economy or banking system since inflation had been historically low for decades. For instance, by the time that Bear Stearns collapsed in March 2008, the Fed had already lowered interest rates from 5.25% in August 2007 to 3.0% in March 2008.10 But times have changed. Just days after the recent bank collapses, on March 22, the Federal Reserve once again hiked interest rates (this time by 25 basis points to 5.0%) while it maintained its pace of quantitative tightening. This most recent rate hike, which happened despite signs that higher interest rates were starting to destabilize key parts of the economy, highlights the policy predicament that the Fed has put itself in. By waiting too long to address inflation, which started spiking in early 2022, the Fed must now decide between two crucial mandates—price stability or financial stability. There is no viable path to fix both simultaneously.

Markets

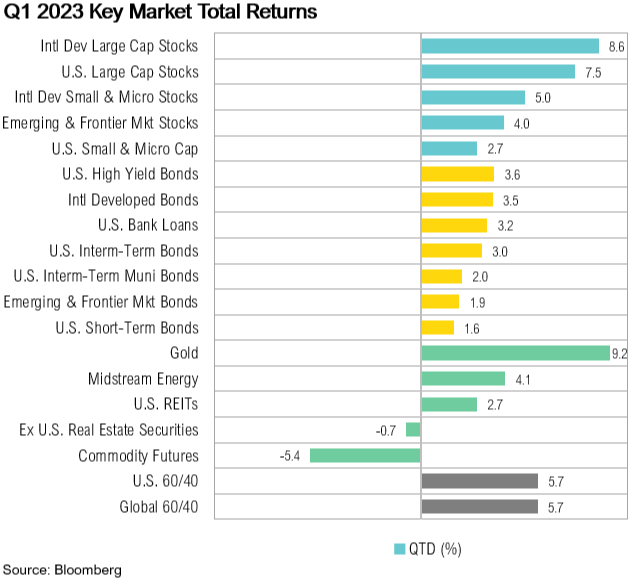

Both U.S. and international equity markets rallied in the last few days of March to end the month (and the quarter) in positive territory. The MSCI EAFE Index ended the quarter up 8.6%, and the S&P 500 posted a respectable 7.5% gain. As longer-term interest rates stabilized, fixed income markets recovered most of the losses made throughout February and ended the quarter at January levels. The Bloomberg U.S. Aggregate Bond Index closed the quarter up 3.0%, while international developed market bonds ended the quarter up 3.5%.

Credit Suisse, the global investment bank and Switzerland’s second-largest bank by assets, finally ran out of time to restore itself as a viable financial institution. In May 2007, the company’s stock price peaked at $72, but from that point forward, it steadily declined. In June 2022, as investors increasingly demanded compensation from the beleaguered bank, Credit Suisse paid 9.75% in interest for a bond offering as a last-ditch effort to raise capital and attract customers.23 Despite this, investors continued to lose confidence in the bank, and in March 2023, its stock price dropped by 70% to less than $1. Subsequently, on March 19, Credit Suisse was bought out by rival bank UBS for 60% less than what the bank was worth two days prior.

On April 2, OPEC+ announced an unexpected cut in oil output of approximately 1.2 million barrels per day, starting in May.The surprise announcement sent oil prices soaring by around 7%, to $85 per barrel. OPEC+ and its allies have cited concerns about weak global demand, as economic growth starts to slow.Meanwhile, the U.S. Strategic Petroleum Reserves have been depleted by more than 222 million barrels since the start of 2022, to a current four-decade low of 371 million barrels.

The new governor of the Bank of Japan, Kazuo Ueda, started his first term on April 8. The country’s next monetary policy meeting is on April 27, and despite widespread speculation that at least some changes might be made to Japan’s ultra-easy monetary policy stance, it seems that Ueda is determined to stick to his predecessor’s stance, stating at a recent press conference that the bank “will be continuing the current easy monetary policy”. Over the past six months, the BoJ has spent over $950 billion in quantitative easing efforts. Even with Japan’s inflation reading at 3.5%, near the previous month’s four-decade high, it seems that Japan’s policy, which has remained virtually unchanged for more than two decades, is not yet out of time from a policymaker’s perspective.

The clock was ticking elsewhere as the popular social media platform TikTok faced a possible ban in the U.S. On March 23, TikTok Chief Executive Officer Shou Chew was grilled before Congress by lawmakers who believed that the Chinese-owned app should be banned in the U.S., citing possible national security threats. Ironically, just a few days later, in testimony to U.S. Senate Committee on Banking, Housing, and Urban Affairs on recent bank failures, Vice Chair for Supervision Michael S. Barr noted that social media contributed to the SVB deposit run by uninsured depositors.

Looking Forward

Recent bank failures are more of a symptom of the Fed’s rapid rate hiking cycle than systemic solvency risk, but they are causing a sharp contraction in lending, which could help trigger a recession.

Due to persistently high inflation, the Fed has continued to hike interest rates, which has stressed the banking system and slowed the economy. To make matters worse, the Fed Funds futures markets currently projects a 70% chance that the Fed will raise interest rates an additional 25 basis points (to 5.25%) at the May 3 FOMC meeting. Beyond that, predictions begin to shift, and markets anticipate a Fed pause, followed by rate cuts before the end of 2023.

Although there is no predefined path for policy or markets, we remain focused on downside risks. If we are wrong and the economic backdrop is stronger than current data suggests, we will still likely participate in any upside, but to a muted degree. Once visibility improves on rate paths, the economic environment, and S&P earnings, we will begin to reallocate capital to asset classes that provide more upside potential.