In a volatile market, many investors prefer to hold a little more cash than they otherwise would or make investments a bit slower – spreading out the allocation to minimize any adverse impact from sudden market drops. With cash on the sidelines earning little to nothing in return, we’ve started implementing a rolling Treasury strategy with minimal interest rate risk, no credit risk, and a current yield in excess of 2.5%, which could be better or worse depending on the timing of the process.

Here’s how it works:

Excess cash that is not earmarked to be deployed in the short-term is invested in a series of Treasury bills, maturing about one month apart from each other. The initial investment is made in Treasuries maturing in 1,2, and 3 months, with an equal allocation to each. When the first Treasury expires in one month, we roll the proceeds into another Treasury that expires three months forward, reestablishing the 1,2, and 3 month maturity schedule set at the outset.

Although this is an active management service, because of the nature of the instruments and the standardization of the process, we charge a discounted fee to implement this strategy. However, we do have a minimum requirement of $300K. Anything less becomes cost prohibitive.

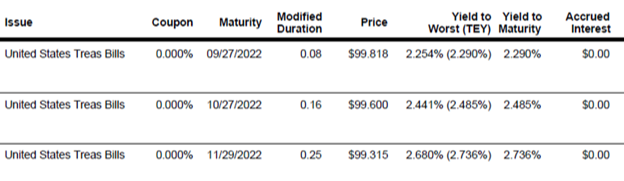

Here is an example of a recent transaction:

We will invest 1/3rd of the total cash into each of the above referenced T-bills. Note that the price of each T-Bill above is below 100 and the stated coupon is zero – implying that the stated yield to maturity is essentially the difference between the price paid and the amount received at maturity. The average yield to maturity of this entire transaction is 2.503%.

When the September T-Bill matures, we reinvest the proceeds into a T-bill maturing in late December if the choice is to continue to roll Treasuries. At the time of this writing, the December T-Bill was yielding roughly 2.9% with a maturity on December 29th. As rates rise, the yield on subsequent investments should continue to increase. An attractive alternative to sitting in cash while waiting to invest.

We caution investors to make sure this cash is not intended to be used within the 3-month period being considered. In the event any of the positions have to be sold before maturity, the price received would be determined by market pricing and may not result in the yield expected.

Benefits

- Higher return than that being paid by banks on savings accounts or CD’s, and higher than the yield on money market investments.

- Discounted management fee

- No credit risk

- Exempt from state and local taxes

Risks

- Prices can still fluctuate from purchase to maturity

- Interest rate risk – rapid rise in short-term rates could lead to missed opportunity cost.

- Opportunity cost of potential returns in equities or higher yielding fixed income

If you have some cash lying idle not generating a decent return while you wait to deploy that capital, why not squeeze out a few extra percentage points above what a bank CD or savings account is currently paying? We can essentially lock in the yield at the time we make the investment for each security – unless of course the US government defaults.